Press

Coreless Banking Provider XYB to Help Modernise Core Banking with IBM

4 min read

Given the number of solutions available and the cost and complexity of building one from scratch, banks would be better served by acquiring a 3rd party core banking solution. One that is proven with existing customer implementations and designed for flexibility to meet the varying requirements across different banks, geographies, customer segments and products. However, choosing a new core banking solution, whether to replace or modernise a bank's existing core banking platform, is a challenging decision. Banks now have an array of potential vendors to choose from, all of which come with different considerations.

The Incumbents Quick Fix / is the fastest route to a bank’s next legacy

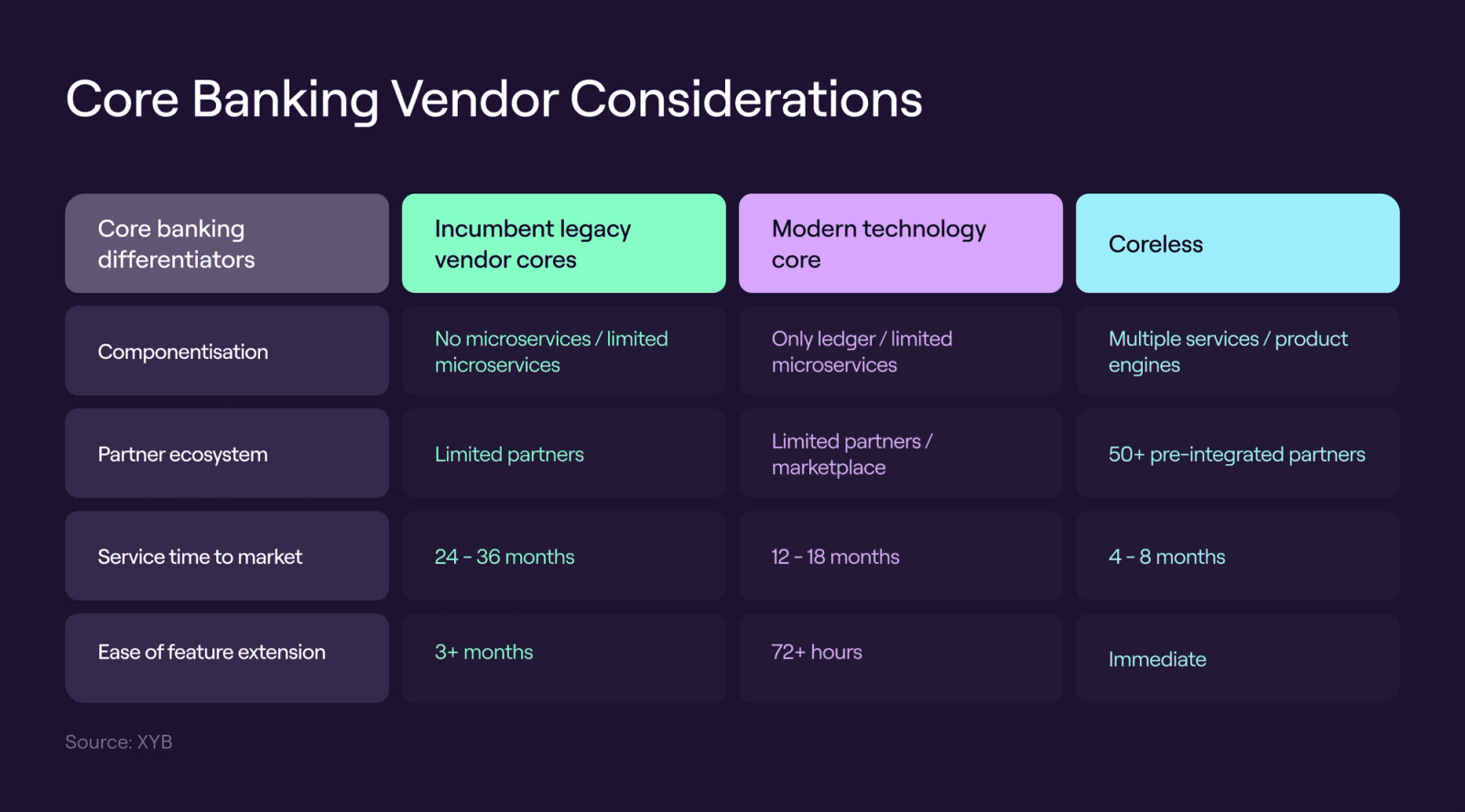

Although traditional incumbent vendors offer a comprehensive breadth of offerings and benefit from long-term relationships with their bank clients, they tend to offer standard ‘one-size-fits-all’ services.

In the transition from mainframe to client-server models, packaged solutions from core banking vendors seem attractive at face value, promising to be more accessible, quicker and cheaper to implement. Their core banking suite is often a mix of acquisitions and in-house developed solutions. Thus, they are a “potpourri” of solutions, technologies, and capabilities developed in different ways. As these suites broaden in their capabilities, internal competition for development budgets makes it difficult for every product to keep up with modern technologies, let alone compete with best-of-breed solutions for their functionality.

These solutions have become the new legacy cores where options are limited by their dependence on old parameters and libraries of predefined product features. To provide a complete solution and to ease implementation, the individual solutions have complex integrations, making it difficult to replace individual functional components.

Another handicap comes when banks want to explore services from third parties. While some incumbents are beginning to offer API marketplaces, others can only tap into a limited number of partners, inhibiting bank choice even further.

These solutions can be deployed on-premise or in the cloud. However, they are not designed for the cloud even if marketed as “cloud native”. Essentially, they are “monoliths in a container”, a monolithic deployment where all the components have been integrated, tested and deployed together. Only the licences determine what the bank can actually use. This makes it easier for the vendor to manage and deploy their suite of solutions but makes it more expensive and complex for banks to handle.

An added handicap is that they have locked-in contracts and extensive maintenance requirements. Banks that are locked into those vendors with long-term contracts can only sit and watch as more agile rivals get to pick and choose which services they want from a variety of vendors.

For digital-only neobanks in particular, these incumbent vendor solutions may not be optimal for their needs. They don’t need the same product sets as traditional banks and won’t be dealing with the same customer use cases, volumes, and throughputs. As such, these players favour core systems that support flexibility, scalability, resilience, and ease of integration for new services.

Modern Core Banking / The new monoliths in smaller packages?

As with the client-server era of technology, the internet era brought in new capabilities also. Aside from the user interfaces moving to browsers or apps, server-side technologies have vastly improved. Previous iterations of technology have always allowed software to be modularised or componentised. However, typically, they would have been deployed as a single monolith or had to be developed on a standard technology that allowed separate components to interact.

With the advent of microservices, components can not only be developed and deployed separately but each component can also be managed separately. This means a component can be upgraded without the whole solution being stopped. It means that machine resources can be allocated appropriately to each component rather than broadly allocated for the entire solution, making the solution much more efficient and cheaper. Each component no longer needs to run on the same machine or the same network; they can be run anywhere and interact with other components using modern API technology. This technology was born out of the internet and makes it possible to run components on different technologies (hardware, operating systems, databases and programming languages) and interact with them as if they were developed on the same machine/technology.

This new generation of core banking providers embraced cloud, APIs, Banking-as-a-Service (BaaS), and financial service componentisation. Their use of microservice architecture to mix and mesh with existing core banking systems is a significant departure from incumbent vendors.

These modern core solutions do not provide the same breadth, geographic reach, or number of client implementations for assurance as incumbent vendors. Much of the breadth of incumbent functionality is now dated and lacks flexibility, so it is no longer an advantage. However, they share something in common with the incumbent cores: although they are developed as components microservices, adopting such a solution means a commitment to the whole platform and not just the functions the bank may need to modernise. Some modern core solutions only focus on the ledger, while others provide, at minimum, a product management suite and the ledger.

A radical core banking transformation is not without risk – but choosing the right vendor with the right execution strategy promises multiple and long-lasting returns.

These modern cores have improved core banking with new technology but have yet to necessarily re-invent core banking. It means that implementation is still risky, complex and costly as it requires replacing a banks ledger and product management capability.

Re-inventing Core Banking / Coreless

Whatever your definition of core banking is, at minimum, in the past, this has meant the ledger and product management (the ability to define and execute financial products). The idea of Coreless banking was borne out of the banking standards group BIAN.

BIAN defines the functional capabilities a bank needs to run, including operational areas like marketing, sales and HR. BIAN defines a set of services spanning the entire bank. These services can be provided by one or more vendors or developed by the bank. The premise is that nothing is dependent on a specific component; everything is exchangeable.

Recognising these components need to share data, and that these contracts can not be universally agreed upon fully, orchestration solutions can be used to map data from one component to another. The critical point is that core banking is now a suite of components, and suppliers can specialise or provide many or all of the components a bank needs. However, there is no dependency on a “core” any more.

After a shaky start and over a decade of evolution, we see global interest in adopting Web 3.0 and digital assets. There are now very few countries that are not preparing for the adoption of central bank digital currencies and, like Europe, providing regulations and guidance on the adoption of cryptocurrencies. There are already solutions for digitising physical assets so that things like artwork or homes can be sold as fractional investments, just like we invest in companies today with shares. This requires a core that can support digital assets, not just currency.

So the three key differentiators of Coreless from Modern Core banking vendors are:

Low code / No Code / The next generation of configuration?

Another differentiator among core banking solutions is how they are configured. Incumbent solutions are typically “parametrised” and often provide a graphical user interface to set values for these parameters. Whilst these give good flexibility and ease of deployment, the bank's flexibility is always limited by the parameters provided by the vendor.

Modern core banking solutions are typically headless and provide the ultimate flexibility through programming interfaces (APIs). This means that the bank or their implementation partner can develop anything the vendor has not supplied. Whilst this provides great flexibility, configuration is limited to IT personnel and requires an IT implementation (testing, proving, deployment) which can take time.

The emergence of low-code, no-code core banking vendors

At a time when a shortage of skilled developers is impacting innovation, more banks are looking at using low-code or no-code core banking platforms.

What’s the difference between low-code and no-code? Low code requires minimal coding skills, enabling a developer to customise the solution with a layer of code. No-code means exactly what it says – no coding skills are needed, allowing the manager of the no-code solution to create a product and predefined product options without having to write a single line of code. In a plug-and-play scenario, the product manager can customise each product in whatever configuration they favour and then combine them. No-code/low-code saves time and money, especially on maintenance and development tasks, leaving banks free to focus on innovation and developing new products and services.

Coreless Banking / Transcending Monolith and Mainframe Limitations

We have already discussed how changes in:

I have also previously discussed the challenges banks face with their core banking systems and how they may look at changing them. I have mentioned Coreless Banking in these blogs but have yet to define it properly.

Coreless Banking: Who? When? Why?

The Banking technology standards group BIAN launched the “Coreless Banking” initiative in 2019 as a collaboration between 6 large banks and several technology companies. The launch press release said, “The Coreless Bank initiative aims to promote a more efficient and effective approach to modernising banking software. The collaboration between initiative partners will make it easier for banks to source and adopt new business services. This will solve the perpetual challenges presented by legacy core infrastructure and allow for faster, more cost-effective development of more relevant services for today’s digital-first customers.” You can read more about BIAN here: https://bian.org/.

While we are still determining exactly how the future will pan out, the best approach to technology is to use open technologies and software designed as interoperable components to create the agility to change in any direction

When looking to launch Monese, the founders investigated core banking solutions and found they had many of the challenges we described earlier. However, from a business perspective, they had seen the banking landscape change and knew that something disruptive in banking could only be done by:

Even looking at modern core banking platforms, they realised they had to develop a very different core banking solution, the next generation: Coreless Banking.

What is Coreless Banking

Coreless banking is a solution that is componentised, that is broken down into smaller functionality that can be:

Coreless Technology

Coreless banking solutions follow the MACH architecture: Microservices, API-first, Cloud-native and Headless. While coreless banking is still in its formative stages, it offers transformative potential – allowing banks to decouple from centralised core systems and rigid monolithic code bases to offer distributed services with more flexibility while not compromising reliability or security.

Each microservice has a specific purpose (for example, ledger, credit scoring or card management) with a standard, well-defined interface. Previously, bank products or services would need to interact with a specific ledger to perform functions like product creation, credit scoring or user logins, but coreless banking apps operate independently in a decentralised, distributed network.

Using a decentralised and distributed model means existing services can be modified, and new services can be launched more easily. An orchestration middleware layer can be used to swap new components as technology or business requirements change. As independent components, updates can be done with no disruption to operations. This means developers of banking applications can execute updates or deployments in isolation without affecting other services, components or operations. This also means if one component crashes, it’s unlikely to take the rest of the system down. Beyond this, moving away from restful interfaces to an event-driven architecture based on Kafka also massively reduces the chances of a misbehaving service having a network effect that brings the system down.

Why Coreless Banking?

Coreless banking is helping banks to:

The key takeaway is that coreless banking enables banks to provide new capabilities without a full-scale replacement of their existing core banking systems. They can modernise their banking systems in shorter phases, providing faster time to value whilst reducing operating costs. Legacy core banking systems can be replaced over time without the risk and complexity of doing it in one project.

Conclusion

We know that banking today is very different to what it was 60 years ago. The past 20 years have ushered in the Internet, broadband, 5G connectivity, blockchain, Web 3.0, Open Banking, and real-time payments – all at our fingertips through handheld devices. We’re already seeing the first forays into AI and quantum computing, and we can be sure that the next ten years will unleash even more incredible technological breakthroughs as our digital-first world becomes even more deeply interconnected.

Currently, banks are exploring AI to generate deeper data analytics capabilities and predictive models to enhance personalisation, customer experience, smart routing of requests, and detect anomalies and fraud in real-time. Combining AI with coreless banking could harness data from multiple sources through an orchestration layer, enabling banks to enhance their omnichannel strategies and ensure each customer gets services that exceed their expectations through the channel that suits them best.

Standards like BIAN help both core banking vendors and banks to standardise the components of a complete banking solution. Orchestration tools help transform and map data between components from different vendors or in-house developed by banks. Each component should be able to run within the same cloud or across the clouds. Combined with the unimaginable speed generated by quantum computing, we stand on the threshold of banking being wholly reimagined.

With the speed at which technology is evolving, creative and visionary banks are now preparing for a future where central bank digital currencies (CBDCs) and tokenisation come to the fore. Coreless banking offers a way for banks to easily integrate these advances with a distributed architecture that ensures operations suffer no disruption to existing services.

As digital transformation continues to touch more areas of our lives, ensuring customers have everything they need will require systems that can keep pace and adapt to their fast-changing demands.

We are on the verge of the next evolution in banking, and coreless banking will create unparalleled customer experiences that will sustain banks, improve profitability, and usher in even more wondrous innovations available at our fingertips. While we are still determining exactly how the future will pan out, the best approach to technology is to use open technologies and software designed as interoperable components to create the agility to change in any direction.

Currently serving as the Chief Commercial Officer at XYB, Santosh brings over 20 years of invaluable experience to the realms of core banking, fintech, and information technology. His career has been a testament to a genuine commitment to driving growth, innovation, and success within the industry.