Press

Coreless Banking Provider XYB to Help Modernise Core Banking with IBM

4 min read

Why the time is right to modernise

Nobody ever said that replacing a core system would be cheap or easy, and we highlighted this previously when we discussed the challenges of replacing core banking. Nevertheless, not all projects to replace core banking have been failures. Below, we discuss the different ways that banks have approached core banking replacement and discuss a new alternative approach, modernisation:

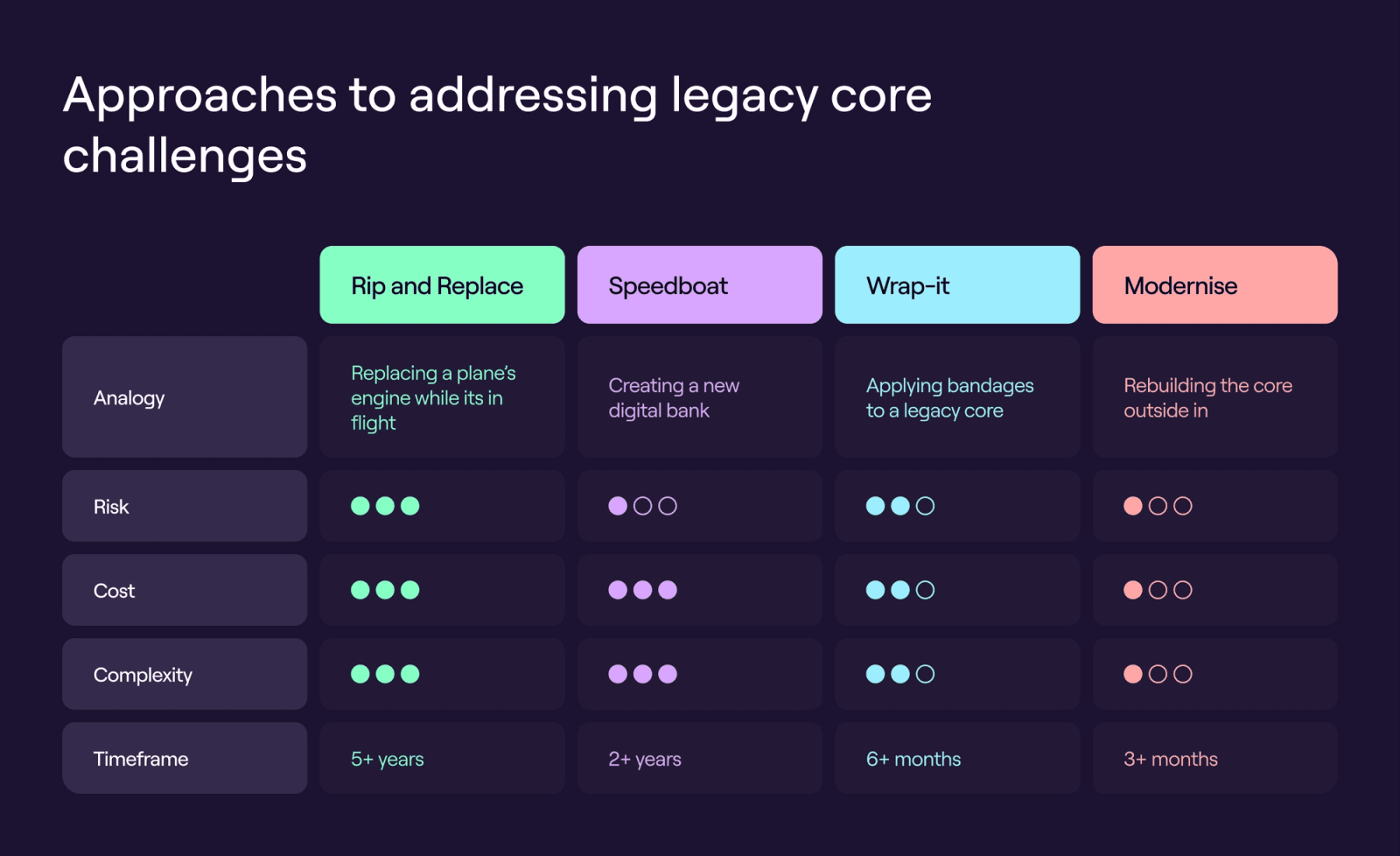

Rip and Replace / Banks replace the core legacy system with a brand new platform or rewrite it entirely on a new tech stack. Typically, the new core runs alongside the legacy system before a complete migration. This option not only requires the new core to be installed, it requires products to be set up identically on the new platform, customer and transaction data to be migrated and systems to be re-integrated with the new core.

The pros…

Leaping to an entirely new system sounds good in theory, but…

The cons…

Speedboat / Create a new branded digital bank. While this competes with the existing bank, it provides the opportunity to create a new technology landscape to escape the legacy decisions of the past. The goal is to create a compelling offering that incentivises existing bank customers to move over.

The pros…

The cons...

Wrap it / banks progressively modernise their core by simplifying, building, and migrating services over time. This approach is not always planned, and banks that have experienced limitations have typically extended capabilities externally on an ad-hoc or silo basis, which is another reason for the so-called “spaghetti architecture” – a technology landscape of many systems integrated or sharing data based on different technologies and providers/in-house.

The pros…

The cons…

Modernise / this involves keeping the core intact as a system of records, posting ledgers and building the required modern functionalities outside it. This can occur in stages, for example, by adding new product management capability to the bank's existing ledgers or just replacing fraud management with a new AI-driven capability. Standards like BIAN can help banks not only categorise and understand their existing technology landscape but then also select appropriate 3rd party components or choose to develop their own. This approach allows banks to take a “best of breed” approach or if they choose to select a vendor with a componentised solution to implement even a full replacement in phases. One of the key differences between this and the previous “Wrap-it” approach is that this option necessitates solutions built on modern architectures (MACH) to leverage technical capabilities for scalability, agility, security and flexibility

The pros…

The cons…

Choosing which approach to adopt depends on banks' specific problems and commercial considerations, including time, cost, deliverability, risk appetite and market opportunity. Multiple core systems could run concurrently in large banks with multiple operational areas spanning different departments (and even countries). That means hundreds or thousands of integrations could be needed using solutions from multiple vendors.

Leaving aside the sheer scale of technical challenges to deal with, the administrative hassle of identifying suitable vendor solutions, performing due diligence and compliance checks, and assessing the feasibility of project modernisation only serves to slow any further attempts at digital transformation.

Grappling with whether to upgrade existing systems or rip them out completely is even more of a struggle when fluctuating macroeconomic cycles can mean budgets get frozen or slashed altogether. With investment, consumer spending, and liquidity battered over the last few years in the wake of Covid and other geopolitical shocks, cost savings have understandably been the priority for banks. But in a period of rising interest rates and thus more revenues for banks, the cost to replace will be easier to afford. These projects can take years, and a leadership change can affect project success or even continuation.

Forward-thinking banks will follow the adage of ‘make hay while the sun shines’ to plough revenues into IT modernisation projects. Modernisation projects that are goal-specific, like “Improving products agility” or “Reducing fraud”, will mean that scope can be clearly defined, managed and implemented more easily and successfully.

Currently serving as the Chief Commercial Officer at XYB, Santosh brings over 20 years of invaluable experience to the realms of core banking, fintech, and information technology. His career has been a testament to a genuine commitment to driving growth, innovation, and success within the industry.